-

Fortress Brokerage

Fortress Brokerage

Medicare Solutions

Ashleigh Baratta

Ashleigh Baratta is a graduate of Georgia State University in Atlanta, GA, where she obtained two Bachelor degrees; one in Journalism and the other in Political Science. Immediately after college she decided that insurance would be the field that she would find the most passion for and she became a resident insurance agent in Georgia for life and accident & sickness. She takes great pride in assisting individuals in their financial and retirement matters as well as their health care. She focuses on insurance for life, disability, annuity, long term care and Medicare. Ashleigh is a member of the National Society of Leadership and Success where she was awarded the National Engaged Leader award. She enjoys cooking Italian food and playing cribbage.

Medicare Fact Finder

Frequently Asked Questions

Medicare is our country’s health insurance program. Although most commonly used by people age 65 or older, some younger people are eligible for Medicare, too. Those include people with disabilities, permanent kidney failure and amyotrophic lateral sclerosis (Lou Gehrig’s disease). Medicare helps with the cost of health care, but it does not cover all medical expenses or the cost of most long-term care. Medicare has four parts:

See the Centers for Medicare & Medicaid Services for more information.The Medicare program has four parts:

Choosing to sign up for Medicare is an important decision that involves a number of issues you may need to consider. The decision you make will depend on your situation and the type of health insurance you have. You may be able to delay signing up for Medicare Part B without a late enrollment penalty if you or your spouse (or a family member, if you’re disabled) is working, and you’re getting health insurance benefits based on current employment. In most cases, if you don't sign up for Part B when you're first eligible, you'll have to pay a late enrollment penalty for as long as you have Part B. Coverage based on current employment does not include:

More informationRetirement Toolkit (Department of Labor)

Read the official pamphlet, Handbook- Medicare & You for more general information.

Individuals with income more than $85,000 and married couples with income more than $170,000 will pay a larger percentage of their monthly Medicare Part B and D costs based on their income.

More Information

Signing up for Medicare Part B may provide you with additional service and location options.

If you don’t sign up for Part B when you are first eligible:

If you already have Medicare Part A and wish to sign up for Medicare Part B, please complete form CMS 40-B, Application for Enrollment in Medicare - Part B (Medical Insurance), and take or mail it to your local Social Security office. You can also call Social Security’s toll-free number 1-800-772-1213 (TTY 1-800-325-0778) or contact your local Social Security office.

More Information

In most cases, if you don’t sign up for Medicare when you’re first eligible, you may have to pay a higher monthly premium.

More information on Medicare late enrollment penalties:

Anyone who has Medicare can get Medicare prescription drug coverage (Part D). Some people with limited resources and income also may be able to get Extra Help. This Extra Help will help pay for the costs, such as monthly premiums, annual deductibles and prescription copayments.

More Information

Monthly Social Security and Supplemental Security Income (SSI) benefits for over 65 million Americans will increase 0.3 percent in 2017. The Social Security Act ties the annual cost-of-living adjustment (COLA) to the increase in the Consumer Price Index as determined by the Department of Labor’s Bureau of Labor Statistics.

The increase will begin with benefits that Social Security beneficiaries receive in January 2017. Increased SSI payments will begin on December 30, 2016.

For more information see:

You can get an original Social Security card or a replacement card if yours is lost or stolen. There is no charge for a Social Security card. This service is free.

You can use a my Social Security account to request a replacement Social Security card online if you:

Other Questions You May Find Helpful

You can get Social Security retirement benefits and work at the same time. However, if you are younger than full retirement age and make more than the yearly earnings limit, we will reduce your benefit. Starting with the month you reach full retirement age, we will not reduce your benefits no matter how much you earn.

For 2016 that limit is $15,720.If you will reach full retirement age in 2016, the limit on your earnings for the months before full retirement age is $41,880..

Starting with the month you reach full retirement age, you can get your benefits with no limit on your earnings.

Use our Retirement Age Calculator to find your full retirement age based on your date of birth.

Use our Retirement Earnings Test Calculator to find out how much your benefits will be reduced.

What counts as earnings:

When we figure out how much to deduct from your benefits, we count only the wages you make from your job or your net earnings if you're self-employed. We include bonuses, commissions and vacation pay. We don't count pensions, annuities, investment income, interest, veterans or other government or military retirement benefits.

Your benefits may increase when you work:

As long as you continue to work, even if you are receiving benefits, you will continue to pay Social Security taxes on your earnings. However, we will check your record every year to see whether the additional earnings you had will increase your monthly benefit. If there is an increase, we will send you a letter telling you of your new benefit amount.

When you’re ready to apply for retirement benefits, use our online retirement application, the quickest, easiest, and most convenient way to apply.

When you’re ready to apply for retirement benefits, use our online retirement application, the quickest, easiest, and most convenient way to apply.

If you need to report a change in your earnings after you begin receiving benefits:

If you receive benefits and are under full retirement age and you think your earnings will be different than what you originally told us, let us know right away. You cannot report a change of earnings online. Please call us at 1-800-772-1213 (TTY 1-800-325-0778) between 7 a.m. to 7 p.m., Monday through Friday, or contact your local Social Security office.

More Information

Your spouse may be able to get benefits if he or she is at least age 62 and you are getting, or are eligible for, retirement or disability benefits. We also will pay benefits to your spouse at any age if there is a child in his or her care. The child must be under age 16 or disabled before age 22, and entitled to benefits. Your spouse also can qualify for Medicare at age 65.

See Retirement Planner: Benefits For Your Spouse for more information.

If you get Social Security benefits or are enrolled in Medicare, you can change your address online by using a my Social Security account.

If you get Supplemental Security Income (SSI), do not have a U.S. mailing address, or are unable to change your address online, you can:

If you do not receive Social Security benefits, SSI or Medicare, you do not need to change your address with us.

COBRA is a law that requires employers with 20 or more employees to let employees and their dependents keep their group health coverage for a time after they leave their group health plan under certain conditions. This is called continuation coverage. You may have this right if you lose your job or have your working hours reduced, or if you are covered under your spouse's plan and your spouse dies or you get divorced. COBRA generally lets you and your dependents stay in your group health plan for 18 months (or up to 29 or 36 months in some cases), but you may have to pay both your share and the employer's share of the premium. Some state's laws require employers with less than 20 employees to let you keep your group health coverage for a time, but you should check with your State Department of Insurance to make sure. In most situations that give you COBRA rights, other than a divorce, you should get a notice from your benefits administrator. If you don't get a notice, or if you get divorced, you should call your benefits administrator as soon as possible.

If you already have group health coverage under COBRA when you enroll in Medicare, your COBRA may end. The length of time your spouse may get coverage under COBRA may change when you enroll in Medicare. For more information about group health coverage under COBRA, call your State Department of Insurance.

If you elect COBRA coverage after you enroll in Medicare, you can keep your COBRA continuation coverage. If you have only Medicare Part A when your group health plan coverage based on current employment ends; you can enroll in Medicare Part B during a Special Enrollment Period without having to pay a Part B premium penalty. You need to enroll in Part B either at the same time you enroll in Part A or during a Special Enrollment Period after your group health plan coverage based on current employment ends. However, if you have Medicare Part A only, sign-up for COBRA coverage, and wait until the COBRA coverage ends to enroll in Medicare Part B; you will have to pay a Part B premium penalty. You do not get a Part B special enrollment period when COBRA coverage ends. State law may give you the right to continue your coverage under COBRA beyond the point COBRA coverage would ordinarily end. Your rights will depend on what is allowed under the state law.

Remember, enrolling in Medicare Part B will also trigger your Medicare Supplement open enrollment period.

If you are age 65 or older and have Medicare and COBRA continuation coverage, Medicare pays first. If you or a family member has Medicare based on a disability and COBRA coverage, Medicare is the primary payer. However, if you or a family member has Medicare based on ESRD, the COBRA coverage is the primary payer and Medicare is the secondary payer for the first 30 months.

Many consumers qualify for additional coverage through Medicaid due to low income status or certain health conditions. In some states, CMS and the state run a demonstration program called a Medicare- Medicaid Plan (MMP) where individuals receive both Medicare Parts A and B and full Medicaid benefits. Generally, qualified individuals are passively enrolled into the state’s coordinated care plan with the ability to opt-out and choose other Medicare options. Designed to manage and coordinate both Medicare and Medicaid and include Part D prescription drug coverage through one single health plan, MMP demonstrations and eligible populations vary by state.

A Health Maintenance Organization (HMO) is a type of Medicare Advantage Plan in which members select a primary care physician (PCP) to help coordinate their care and must go to providers in the Plan’s contracted network, except for emergency, urgent care, and renal dialysis services. Members will need referrals from their PCP to see specialists in some plans.

IMPORTANT: Out-of-network providers are not required to accept the plan’s terms and conditions of payment; therefore, the member may be responsible for the full cost of services.

A Preferred Provider Organization (PPO) is a type of Medicare Advantage (MA) plan in which the member can use either network providers or non-network providers to receive services (going outside the provider network generally costs more). The plan does not require member to have a referral for specialist care. IMPORTANT: Out-of-network providers are not required to accept the plan’s terms and conditions of payment; therefore, the member may be responsible for the full cost of services.

A Point-of-Service (POS) is a type of Medicare Advantage HMO plan that gives members the option to use provides outside the plan’s contracted network for certain benefits, generally at a higher cost. The benefits that are covered out-of-network vary by plan; some plans may have coverage limits for certain benefits. Our-of-network providers are not required to accept the plan’s terms and conditions of payment; therefore the member may be responsible for the full cost of services. Members will need referrals from their PCP to see specialists in some plans.

A Private Fee-for-Service (PFFS) is a Medicare Advantage (MA) plan that allows members to go to any Medicare eligible provider who agrees to accept the PFFS plan’s terms and conditions of payment. PFFS Plans may or may not use networks to provide care, depending on whether the PFFS Plan is a network or non-network plan.

A Special Needs Plan (SNP) is a Medicare Advantage (MA) plan that provides health care for specific groups of people, such as those who have both Medicare and Medicaid (dual SNP), or those who reside in a nursing home (Institutional SNP), or those who have certain chronic medical conditions (Chronic Condition SNP).

A Medical Savings Account (MSA) is a Medicare Advantage (MA) plan that combines a high deductible MA plan and a bank account. The plan deposits money from Medicare in the account. Members can use it to pay for their medical expenses until their deductible is met.

An Out-of-Pocket (OOP) Maximum is a feature that limits the amount of money that consumers will have to spend on certain health care services throughout the year. Once members reach the OOP maximum for covered services, they do not have cost sharing for any additional services that are included in the OOP maximum for the remainder of the year.

The OOP maximum amount can and does vary between Medicare Advantage plans and change each year.

All consumers with Medicare can obtain prescription drug coverage. Private insurance companies provide these plans.

Each plan can vary in cost and drugs covered. Consumers can access their Medicare Part D benefits by enrolling in either a stand-alone PDP or by joining a Medicare Advantage Prescriptive Drug plan (MA-PD). Other consumers may receive Part D benefits through an Employer-Sponsored Group Retiree Plan.

Member will pay a monthly premium to the plan to receive prescription drug coverage. In addition, they must continue to pay Medicare Part B premium, if applicable.

Members have three option to pay their monthly plan premium:

IMPORTANT: As of January 1, 2011, the consumer’s Part D monthly premium could be higher based on their income. This is called the Part D Income Related Monthly Adjustment Amount (Part D IRMAA) and affects fewer than 5% of Medicare consumers.

In the consumer’s modified adjusted gross income as reported on their IRS tax return from two years ago, is more than %85,000 (individuals and married individuals filing separately) and $170,000 (married individuals filing jointly), the consumer will pay extra for Medicare Part D. See: Medicare Premiums: Rules for Higher-Income Beneficiaries Social Sequrity

A member might have to pay a late enrollment penalty if they did not enroll in a Medicare plan with prescription drug coverage when they first became eligible for Medicare and did not have other creditable coverage.

There are Four Stages to Medicare Part D:

Most Medicare eligible consumers can enroll in a Medicare PDP plan, but some enrollees will need extra help to pay for their prescriptions. There is a government program called “Extra Help” that will assist beneficiaries with PDP payments.

People with limited income may qualify for the Low Income Subsidy (LIS) through Medicare’s Extra Help program. The Extra Help can reduce or eliminate the following costs based on a member’s eligibility as determined by CMS:

Qualified enrollees can apply for Extra Help through the state Medicaid office or the Social Security Administration (SSA). People who are approved for Extra Help can usually begin receiving benefits the first day of the month following application.

Based on the Low-Income Subsidy (LIS) level awarded to the enrollee, their monthly plan premiums may be reduced by 25%, 50%, 75% or 100%.

CMS determines the LIS coverage level a beneficiary receives. The LIS benefit amount takes the place of the Part D benefit coverage. Once the beneficiary has Extra Help, they will begin to pay the Low-Income Subsidy cost share (LICS) associated with their level of subsidy. The enrollee’s copayments and coinsurance levels are reduced dramatically at all LIS levels.

The health plans listed below are additional and more uncommon health plans. For more information please click here

The health plans listed below are additional and more uncommon health plans. For more information please click here

PACE uses Medicare and Medicaid funds to cover medically-necessary care and services. Consumers may have either Medicare or Medicaid or both to join PACE.

Enrolling a consumer in a MA plan will automatically disenroll then from their PACE plan or vice versa. Agents should use special caution when disenrolling a consumer from a PACE plan into a MA plan sure to all the additional benefits a PACE program provides.

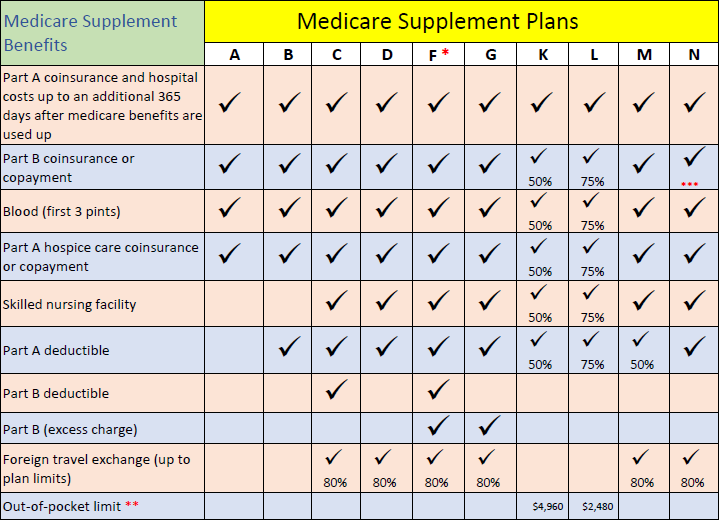

Medicare Supplement Chart